Try our newest merchandise

![[Netflix Certified & Auto Focus] Smart 4K Projector, VGKE 900 ANSI Full HD 1080p WiFi 6 Bluetooth Projector with Dolby Audio, Fully Sealed Dust-Proof/Low Noise/Outdoor/Home/Bedroom](https://i0.wp.com/m.media-amazon.com/images/I/71yY+2ryOZL._AC_SL1500_.jpg?w=300&resize=300,300&ssl=1)

![[Netflix Official & Auto Focus/Keystone] Smart Projector 4K Support, VOPLLS 25000L Native 1080P WiFi 6 Bluetooth Outdoor Projector, 50% Zoom Home Theater Movie Projectors for Bedroom/iOS/Android/PPT](https://i2.wp.com/m.media-amazon.com/images/I/71Emwd78tlL._AC_SL1500_.jpg?w=300&resize=300,300&ssl=1)

Why has the market fallen out of affection with Disney?

Bob Iger is nearing the tip of a multi-year comeback run as CEO and has overseen a number of key enhancements to Disney’s enterprise. Streaming has stopped bleeding money. The corporate has mapped out a serious growth pipeline for parks and experiences. ESPN is bolstering its streaming technique because the pay-TV bundle continues to shrink.

Regardless of this, the inventory is sitting about 43% under its 2021 peak — and it may go away a dent in Iger’s legacy.

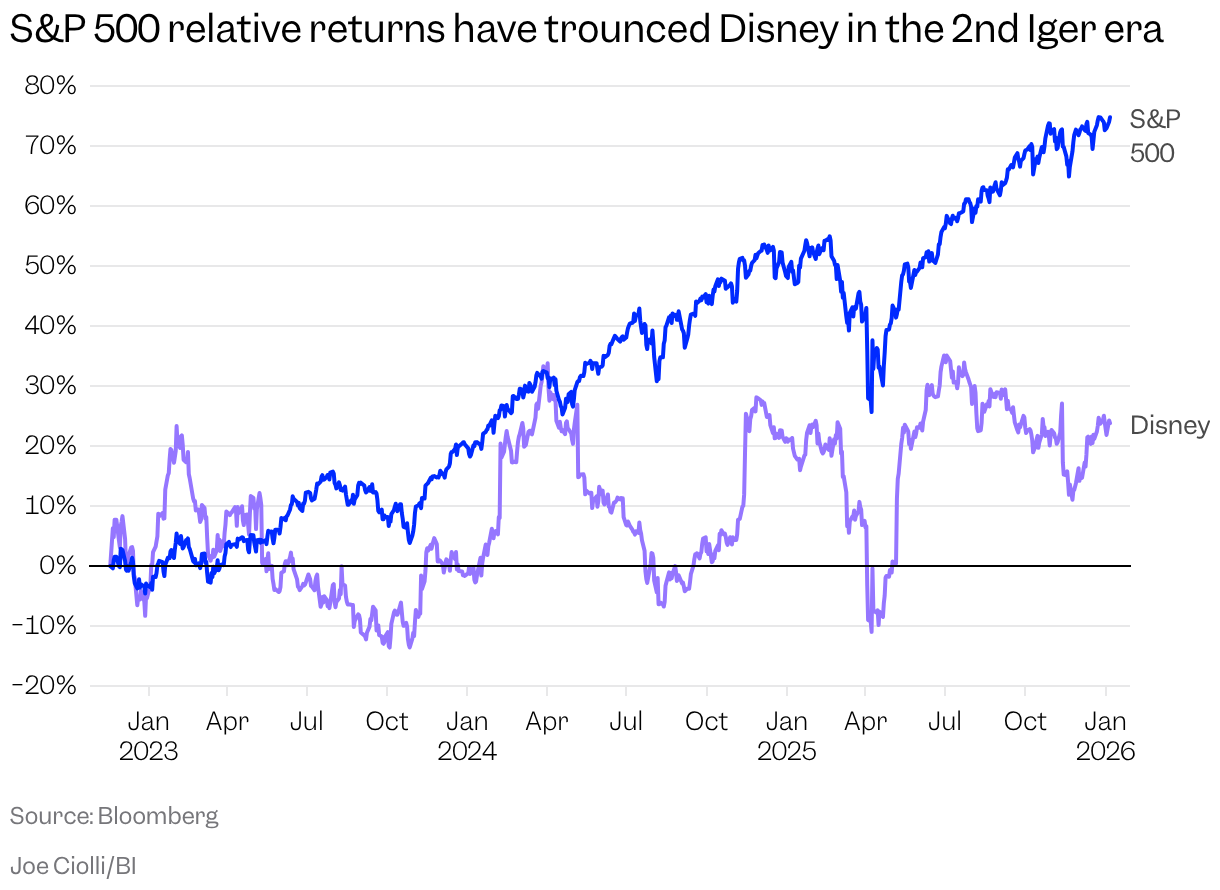

Throughout Iger’s 15-year first run as CEO, which resulted in 2020, Disney’s inventory surged as he reworked the corporate via acquisitions — Pixar, Marvel, and Lucasfilm — that powered its films, TV exhibits, client merchandise, and parks. The introduction of the streaming service Disney+ in 2019 set off a progress narrative that noticed the inventory attain its all-time excessive of $198.60 in March 2021.

Since then, Disney has fallen effectively behind the S&P 500. Disney is buying and selling round $114 — up about 24% from the beginning of Iger’s second time period as CEO. By comparability, the S&P has gained round 75%.

“Disney was the one inventory in media that you would evaluate to everybody else,” longtime Financial institution of America analyst Jessica Reif Ehrlich stated, referring to the broader market. “That is the bottom relative valuation it is had in additional than 40 years.”

Disney is working inside a sophisticated setting for media giants throughout Iger’s second run, which is mirrored within the various inventory efficiency of its opponents. Disney has no actual peer, however shares of its largest rival, the pure-play streamer Netflix, have gained practically 206% since November 2022, when Iger returned to Disney. Warner Bros. Discovery — which features a storied Hollywood studio and HBO — was lagging till takeover curiosity fueled a inventory run. Its shares are up 165% in that point interval. Shares of NBCUniversal proprietor Comcast, which is coping with each a troubled cable enterprise and a sub-scale streamer, have declined about 12%.

Disney workers and on a regular basis buyers who spoke with Enterprise Insider stated they have been annoyed by the inventory’s efficiency, however most believed it will finally rebound.

“The basics are there, and whereas the inventory has lagged, it is a part of a diversified portfolio, so I can afford to attend it out,” stated Dia Adams, a Disney fan and journey agent.

So, what’s holding again the inventory?

Wall Road analysts describe Disney as comprising three separate however interconnected companies, every with its personal distinct danger profile. At any given time, one among them seems shaky sufficient to hamper Disney’s total progress story.

Leisure: migrating towards a questionable streaming future

Disney’s Leisure division, which spans linear TV networks, streaming providers, and studios, is essentially the most advanced piece. Income from Disney’s conventional TV enterprise continues to say no as viewers shift away from the medium. That was on full show in Disney’s fiscal fourth quarter ending September 27, with linear working revenue falling 21% 12 months over 12 months.

The streaming enterprise has been a vibrant spot, with working revenue up 39% 12 months over 12 months within the fourth quarter. Nevertheless, skeptics are involved about streaming’s means to interchange linear TV’s decline and level out that progress is more and more coming from outdoors the US, the place persons are typically extra price-sensitive.

Jamie McCarthy/Getty Photos for Disney

The streaming wars may additionally get harder for Disney shifting ahead. Netflix and Paramount Skydance are in a bidding warfare over Warner Bros. Discovery, and whichever mixture emerges will create a bigger rival that would put stress on Disney.

Then there’s Disney’s studio enterprise: hit-driven and costly.

Wall Road was searching for Iger to work his magic on the film enterprise, and the movies have been “horrific” in Disney’s 2025 fiscal 12 months, Ehrlich stated. The corporate blamed a decline in studio income on comparisons to the prior 12 months’s “Deadpool & Wolverine” and “Inside Out 2.” Issues have been wanting up, although, with the blockbuster efficiency of “Zootopia 2” on the field workplace.

Experiences: a money-printing machine being pushed arduous

The Experiences division encompasses theme parks and cruise ships, and has turn out to be a prime driver of revenue for Disney. The division’s current power has relied closely on worth will increase reasonably than a bump in attendance.

That raises a key query: How a lot pricing energy does Disney have left?

In 2025, home park attendance decreased 1%, in keeping with Disney’s annual report. Disney has additionally confronted issues about competitors in Florida from Comcast’s lately opened Epic Universe, and in regards to the delayed debut of Disney Journey in Singapore, now scheduled for March.

VCG/VCG through Getty Photos

Sports activities: a progress story hampered by rising prices

Sports activities is the smallest phase of Disney’s enterprise by income, however it has a transparent progress story.

ESPN is modernizing for streaming with a newly enhanced app and large direct-to-consumer ambitions. That stated, the price of sports activities rights is growing, and competitors is intensifying — not solely from conventional rivals like Fox, but in addition from deep-pocketed tech firms similar to YouTube and Amazon.

Disney’s sports activities spending was a subject on its newest earnings name after it paid greater than a 73% enhance for NBA rights in its newest deal, which kicked off with the 2025-2026 season. The corporate stated the worth to audiences and advertisers was large, even when the associated fee creates some “bumpiness” in monetary outcomes.

How a lot does the brand new CEO matter?

Wall Road sees no fast repair for Disney’s inventory. Analysts need proof of regular, repeatable earnings progress, whether or not from a stronger movie slate, improved streaming profitability, or an anticipated carry from the cruise enterprise in late 2026.

The inventory worth issues in ways in which have an effect on Disney operationally. Fairness is vital to retaining prime executives, and stagnant shares can uninteresting the attraction of stock-based pay. This might complicate the job of Disney’s subsequent CEO.

Selcuk Acar/Anadolu through Getty Photos

Disney’s CEO succession has turn out to be a favourite parlor sport, with chatter centering on Experiences chief Josh D’Amaro and Disney Leisure co-chair Dana Walden.

No matter who’s chosen, buyers are hoping for regular management over reinvention. The need for continuity limits Iger’s means to make sweeping adjustments in his remaining months.

“Usually, CEOs will strive very arduous to exit on a excessive notice,” stated Laurent Yoon, US media and telecom analyst at Bernstein. “For Iger, it is definitely not good. It is going to be tough to get inventory in a very good course, no less than close to time period.”

![[Win 11&Office 2019] 14″ Rose Gold FHD IPS Display Ultra-Thin Laptop, Celeron J4125 (2.0-2.7GHz), 8GB DDR4 RAM, 1TB SSD, 180° Opening, 2xUSB3.0, WIFI/BT, Perfect for Travel, Study and Work (P1TB)](https://i3.wp.com/m.media-amazon.com/images/I/71CzO7Oc8jL._AC_SL1500_.jpg?w=300&resize=300,300&ssl=1)